Estate Planning / Legacy Life Insurance

Life Insurance for Estate Planning / Legacy

How is Life Insurance used in Estate and Legacy Planning

Life insurance in estate and legacy planning provides liquidity, meets tax obligations, equalizes inheritances, funds trusts, and supports charitable goals by delivering a predictable, generally income-tax-free death benefit.

Estate liquidity: Pays estate taxes, final expenses, and debts so other assets (illiquid holdings like real estate or a business) don’t have to be sold quickly.

Estate tax planning: Life proceeds can be used to cover estate tax liabilities, preserving the value of the estate for heirs.

Irrevocable Life Insurance Trust (ILIT): Placing a policy in an ILIT keeps proceeds out of the taxable estate, provides creditor protection, and gives control over distribution timing and amounts.

Wealth replacement/equalization: Replaces wealth given to charity or to one child so other heirs receive equivalent value without splitting specific assets.

Business succession: Funds buy-sell agreements and provides heirs with cash for business interests to prevent forced sales.

Care for surviving dependents: Provides income replacement or a lump sum for children, disabled family members, or a surviving spouse.

Special needs & supplemental income planning: Pays for lifetime supplemental benefits without disqualifying beneficiaries from means-tested government programs (when structured properly).

Charitable giving: A policy can name a charity as beneficiary or be owned by a charity-designated trust to fund legacy gifts and potentially provide current tax benefits.

Estate equalization: Allows an executor to leave illiquid or sentimental assets to certain heirs while compensating others with insurance proceeds

Typical Structures:

Owner/insured/beneficiary choices: Who owns the policy (you, your trust, or a third party), who’s insured, and who receives proceeds affects tax exposure and control.

ILIT mechanics: Trust owns the policy; premiums are paid via annual gifts to the trust (often using gift-tax annual exclusion); when properly set up, proceeds are not includable in the insured’s estate.

Survivorship (second-to-die)policies: Insure two spouses; pay only after both die—commonly used to fund estate taxes while keeping single large-tax-free payments until the second death.

Policy life-cycle in planning: Purchase → name/structure ownership and beneficiary → coordinate with wills/trusts and buy-sell agreements → review periodically for changes in health, tax law, or family circumstances.

Tax & legal considerations (general)

Death benefits are generally income-tax-free to beneficiaries, but proceeds may be included in estate value if the insured retained incidents of ownership.

Premiums are usually paid with after-tax dollars; gifting premiums into an ILIT requires careful compliance with gift-tax rules and Crummey notices to qualify for exclusions.

Survivorship policies can reduce total premium cost but delay liquidity until both lives end.

State and jurisdictional rules, and changing tax law, can materially affect outcomes — professional tax and estate counsel is recommended.

Practical steps to implement

Identify liquidity needs at death (taxes, debts, business transfer, family support).

Choose policy type (term, whole, universal, survivorship) based on horizon and cash-value needs.

Select ownership/beneficiary vehicle (personal ownership, ILIT, revocable trust, company).

Coordinate with estate documents (will, trusts, powers of attorney).

Fund premiums and document gifting if using an ILIT.

Review every 3–5 years or after major life events.

Charitable Giving using Life Insurance

Ways life insurance can support charitable giving

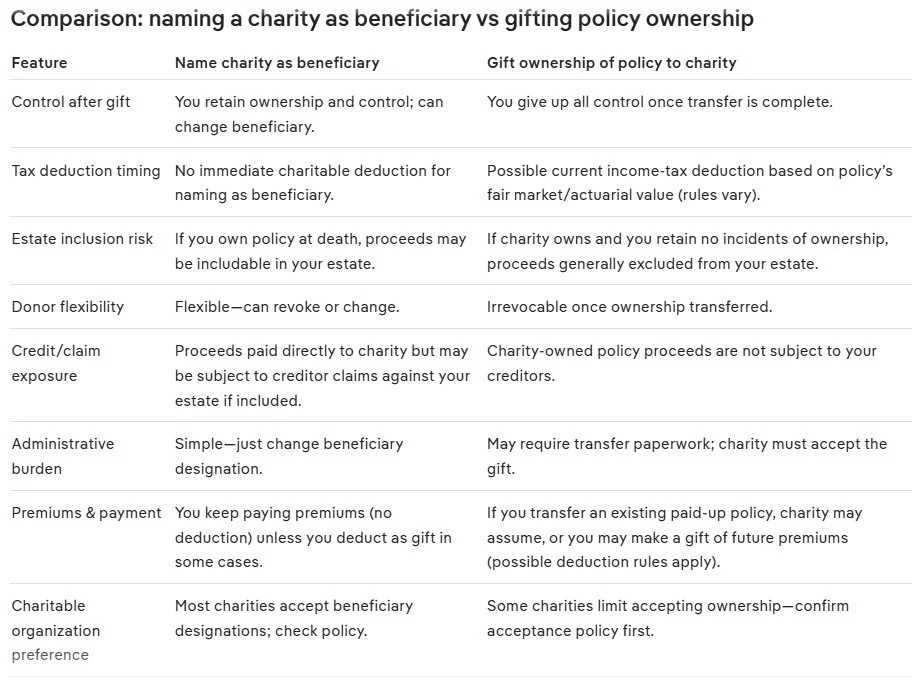

1) Name a charity as beneficiary

Charity receives the policy’s death benefit directly (income‑tax free).

You retain ownership and can change the beneficiary unless you assign the policy.

2) Make the charity the policy owner

Charity owns and receives proceeds; you may be eligible for an immediate charitable income-tax deduction for the policy’s value (rules vary).

The charity controls the policy; you cannot change it later.

3) Gift a paid-up policy

Transfer ownership of an existing paid-up policy to a charity now; the donor may get a current deduction based on actuarial value.

4) Use an Irrevocable Life Insurance Trust (ILIT) with a charitable component

ILIT holds the policy to keep proceeds out of your taxable estate and can direct funds to charities and heirs per the trust terms.

5) Charitable remainder trust (CRT) funded with policy/cash value

A CRT can receive policy proceeds or transfer cash value; provides income to non-charitable beneficiaries for life/term, then remainder to charity, often yielding current tax benefits.

6) Single-premium policy to fund a future gift

Buy a policy and name a charity beneficiary; relatively small premium today can create a larger future gift.

Benefits

Large, predictable future gift regardless of investment performance.

Potential current tax deductions (when charity owns/receives a gift of the policy).

Keeps other assets intact for heirs.

Can leverage relatively small premiums into a sizable charitable impact.

Practical steps

Decide desired charitable outcome (immediate gift vs legacy).

Choose structure (beneficiary designation, charity owner, ILIT, CRT).

Confirm charity’s policy-acceptance rules.

Model costs, gift value, and tax effects with an advisor.

Document the arrangement and coordinate with estate plans

Get Started Now

Submit form, Call, text, or email us.

This Life Submit Form is the minimum information necessary,